You are at 585. You need $15,000. The lender's pre-qualification page is dangling a 29.99% APR in front of you, and there is a voice in your head asking whether to take it now or spend six months getting your file to 680 first.

I am going to run the math on both. With real numbers. Not a vibe.

Why this comparison matters more than your marketing-page APR

Most rate articles publish averages by tier and stop there. That is fine if you want to know what the market looks like. It is useless when you are deciding between borrowing now and waiting. The decision lives in dollars: how many more dollars total you pay over the life of the loan.

The Truth in Lending Act (Reg Z, 12 CFR 1026.18) requires every lender to disclose the APR, finance charge, and total of payments in a boxed disclosure on the offer. That box is the only number that matters for this comparison. Not the marketing rate. Not the headline. The box. Our walkthrough on how to read a personal loan disclosure box the way a regulator does takes the box apart line by line.

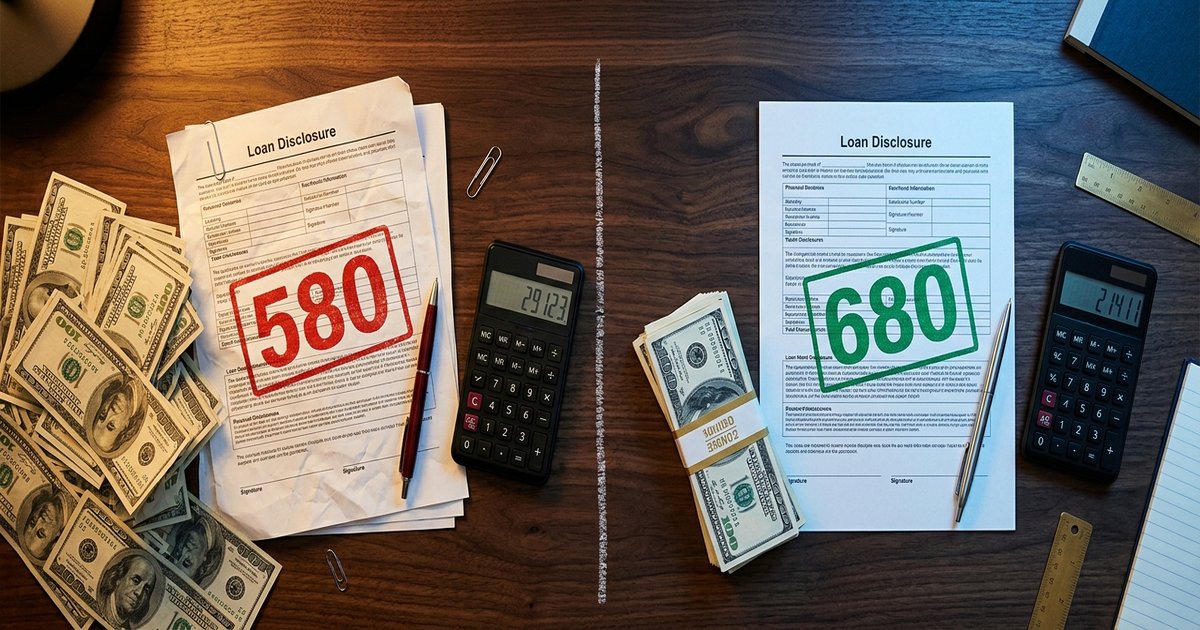

The two example loans, side by side

Let's stick with $15,000 of principal and a 60-month (5-year) term. Same loan amount, same length, only the APR changes.

680 FICO at near-prime APR

For borrowers in the 670 to 739 "good" credit band, current 2026 averages cluster between 12% and 18% depending on lender mix. Source: Bankrate, average personal loan rates April 2026.

Use 14.99% APR. Fixed-rate, 60-month, $15,000 principal:

- Monthly payment: about $356.85

- Total of payments: about $21,411

- Total interest paid: about $6,411

580 FICO at near-subprime APR

Below 630, average APRs jump to 21.65% and routinely climb to the federal cap of 35.99% at the lenders that will fund this tier at all.

Use 29.99% APR. Same principal, same 60-month term:

- Monthly payment: about $485.39

- Total of payments: about $29,123

- Total interest paid: about $14,123

The difference

$7,712. Total. Over five years.

That is the cost of waiting too late or applying too soon. Almost the price of a used Honda Civic in interest, on the same $15,000 loan, for the same 60 months, because of one number on a credit pull.

Where the math gets worse for the 580 borrower

The APR alone undersells the gap. Three things make the bad-credit loan more expensive than the disclosure box first suggests.

Origination fees. Subprime personal loans commonly carry 5% to 8% origination fees taken from the Amount Financed. On a $15,000 gross loan with an 8% origination, you receive $13,800 in cash but make payments on the full $15,000. The effective APR is higher than the disclosed APR. Our piece on the hidden origination fee math shows why a higher-stated APR with no fee can beat a lower-stated APR with a fee.

That means you have to size the loan to your actual cash need plus the fee. If you need $15,000 in your account, you have to borrow about $16,300 gross. That bumps your monthly and your total interest above the numbers I just ran.

Late-fee math. A $25 late fee on a $485 monthly payment is one thing. The same fee on a thinner-margin household budget compounds, because the next month's autopay can fail, fees stack, and the lender reports a 30-day late to the bureaus. That single late report can drop a 580 file another 60 to 90 points. Now you cannot refinance out at any rate.

Approval itself. Below 580, approval rates at most prime lenders sit under 1%. So the "gap" between 580 and 680 is sometimes not lower rate vs higher rate. It is approval vs no approval at all.

The six-month plan that closes the gap

Lifting a file from 585 to 680 in six months is plausible, not guaranteed. It requires a few moves stacked together.

Pay utilization down before statement close, not before the due date. Card issuers report on the statement closing date. Federal regulation requires at least 21 days between statement close and payment due. Pay each card down to under 10% of its limit before the statement cuts and you change the snapshot the bureaus see. This single move accounts for most of the lift in 30 to 60 day windows because amounts owed is 30% of the FICO calculation. Our companion piece on three credit score moves that actually work in 60 days walks through the timing.

Dispute clear errors. Pull all three reports through the CFPB's credit reports resource or directly at AnnualCreditReport.com. Look for collections that should be paid, accounts that are not yours, late marks the creditor cannot validate. File disputes online. Bureaus have 30 days to investigate under FCRA.

Keep on-time payment streaks alive. Payment history is 35% of the score and it heals slowly. Six months of clean autopay is six months of compounding repair.

Do not open new accounts. Every new card or loan adds a hard inquiry and lowers your average account age. Both pull the score the wrong way for at least the first six months.

Borrowers describe going from the high 500s to the high 600s in three to four months by stacking these moves. I do not promise that. I am telling you what the lever looks like.

When borrowing now is still the right call

Sometimes the math says wait, and the situation says no. Three cases where I would not delay six months even at 580:

Genuine emergencies. Medical bills hitting collection, a furnace replacement in January, a car repair that determines whether you keep your job. The cost of waiting is not "$7,712 in extra interest," it is "I lose income, the credit score drops anyway, and I am worse off in 60 days than today." Our emergency loan decision tree sorts your options by deadline.

Refinancing higher-rate debt. If you are servicing $15,000 in payday or title loans at triple-digit APRs, even a 29.99% personal loan is a step down. The comparison stops being 580 vs 680 and becomes 30% vs 200%.

Opportunity cost. Tools to start a side business that produces real income inside 12 months can outrun the interest cost. That is a judgment call. Be honest with yourself about the income, not the dream.

How to read your prequalification offer to know which tier you are in

The prequalification offer (soft pull, no score impact) is the lender showing its hand. Three lines on that offer tell you where you actually sit:

- APR range. If the lender quotes you a single number, that is your tier. If they quote a range and you sit at the high end of it, you are at the bottom of their accepted credit band.

- Origination fee. Zero or 1%: prime tier. 5% to 8%: near-subprime to subprime tier. The fee is the lender pricing risk into the front of the loan.

- Term flexibility. Prime borrowers see 24 to 84 month options. Subprime offers often default to 60 months because longer terms generate more interest.

If the offer says 30%+ APR with a 7% origination, you are sitting in the tier this article is asking you to leave.

State APR caps that change the comparison

National-tier averages do not apply equally everywhere. New York's civil usury cap sits at 16% for most consumer loans. Massachusetts caps personal loans at 20% APR. Connecticut and New Jersey have similar limits on certain unsecured products. Lenders licensed to operate in those states cannot quote a 29.99% APR on a personal loan to a resident, even at 580. Our state rate caps explainer maps the strict and permissive states.

If you live in a capped state, the gap is narrower than the national numbers suggest, but the approval gap can be wider, because lenders simply will not fund subprime files there at all. If you live in an uncapped state (Texas, Utah, Nevada among others), the national numbers may understate what your offer actually looks like.

A quick decision tree

Run yourself through this in five minutes.

- Is the loan need a true emergency (medical, housing, transportation that affects income)? If yes, apply now. Read the disclosure box twice. Pick the longest term you can afford so you can prepay.

- Can you wait 60 days? Pay utilization down before each statement closes, file disputes for any clear errors, do not open new accounts. Re-pull your score. If you crossed 640, re-pre-qualify.

- Can you wait 180 days? Stack the 60-day plan with six months of clean payment history and zero new tradelines. Re-pre-qualify at the 180-day mark. If you cleared 670, the math in this article just saved you several thousand dollars.

- Are you sitting at 580 with a true 50%+ DTI and no income to add? Waiting will not fix this alone. The work is on the income or expense side, not the credit side. Talk to a nonprofit credit counselor (NFCC.org) before adding any new debt.

Trust Point Loans is not a lender. We help borrowers see the loan options that fit their situation, and we run articles like this so you can read your offer before you sign it.

Frequently Asked Questions

Is a 29.99% APR on a personal loan even legal?

In most states, yes. The federal ceiling on most personal loans funded by national lenders is 35.99% APR. State caps vary; New York, Massachusetts, Connecticut, and New Jersey have lower limits on certain products. Federal credit unions cap personal loans at 18% APR.

How much can my credit score realistically rise in 60 days?

FICO does not publish point predictions and any tool that quotes you a specific number is guessing. Stacking utilization paydown, dispute of clear errors, and zero new accounts has produced 30 to 60 point lifts in real-world threads. Your file will respond differently.

What is the actual difference in monthly payment between a 580 and 680 APR on a $15,000 five-year loan?

At 14.99% (a typical near-prime rate) the payment is around $357. At 29.99% (a typical subprime rate) the payment is around $485. That is roughly $128 a month, or about $1,540 per year, in extra cash flow tied up in interest.

Should I take a 36-month term to reduce total interest?

Total interest is lower on a shorter term, but the monthly payment is higher. If a higher payment pushes your DTI past 45%, the lender may not approve you at the better rate. Pick the term that keeps DTI under 45%, then prepay aggressively if your loan has no prepayment penalty.

Does waiting six months to apply hurt me if rates go up in the meantime?

Possibly. Rate environments shift. The Federal Reserve's 2024 to 2026 rate path widened the spread between near-prime and subprime more than it raised the floor for prime borrowers. If you are climbing tiers, you generally still come out ahead even if the broader market moves against you. If you are staying in the same tier, the answer flips.

Will applying at 580 and getting denied hurt my score further?

Yes, by a small amount. A hard inquiry typically costs 5 to 10 points and stays on file for 24 months, though it stops affecting the score after 12. Personal loan inquiries are not bundled by FICO's rate-shopping logic the way mortgage and auto inquiries are, so each personal loan hard pull counts separately.