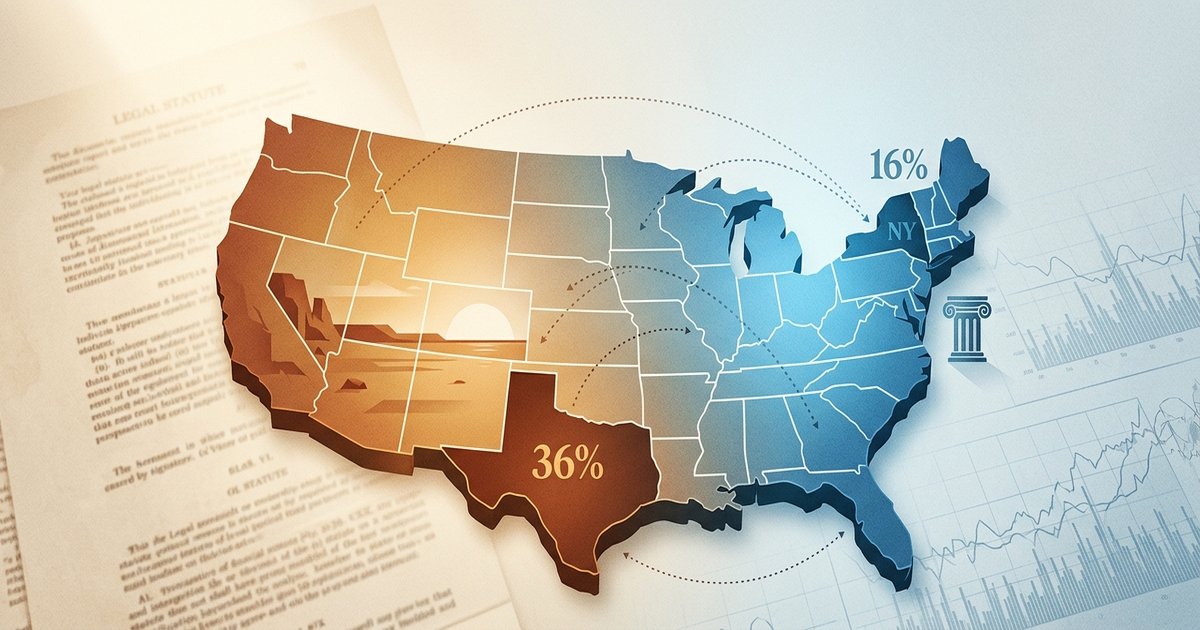

Two borrowers with identical credit files apply to the same national personal loan lender on the same morning. The borrower in Brooklyn gets a quote ceiling of 24%. The borrower in Houston sees an offer with a ceiling closer to 36%. The Mississippi borrower applying through a storefront installment lender on the same day might be quoted 297% APR on a small-dollar loan, and that quote is legal under state statute. Same lender brand, same federal regulatory floor, same applicant profile. Three different ceilings.

The federal government does not set a general usury cap on consumer loans. States do. And the spread between the strictest state and the most permissive is wide enough to change which lenders even operate in your zip code, what rate they can quote, and whether you have a felony backstop protecting you from a 30%-plus loan.

Why two borrowers with the same credit score see different ceilings

Federal law sets the disclosure floor through TILA, and the Military Lending Act caps total APR (MAPR) at 36% for active-duty servicemembers and dependents nationwide. Outside those federal rules, state law sets the ceiling. The result is a layered system: federal disclosure plus state cap plus the lender's own pricing model.

A national lender like SoFi or Upstart caps its advertised personal loan APRs at 35.99% or below in most cases. That ceiling sits below most state criminal usury limits but at or above many state civil caps. So the same lender, applying the same credit model to the same applicant, hits a different statutory ceiling depending on where the borrower lives. The lender can extend the offer in Texas. It cannot extend the same offer in New York without exceeding the criminal usury cap.

The federal floor vs the state ceiling

Federal rules tell the lender what to disclose. State rules tell the lender what it cannot legally charge. Under DIDMCA Section 521, state-chartered banks can "export" their home-state interest rates across state lines, which lets a Utah-chartered bank lend at Utah's permissive rates into New York. Section 525 lets a state opt out of that preemption for loans made within its borders. Iowa, Puerto Rico, and (since July 1, 2024) Colorado have opted out under HB23-1229.

The 10th Circuit ruled in November 2025 that Colorado's 36% APR cap applies to out-of-state state-chartered banks lending into Colorado, narrowing DIDMCA preemption and shifting the playing field for fintech personal loans. That ruling applies in the 10th Circuit. Other circuits may rule differently. The DIDMCA preemption fight is ongoing.

New York: 16% civil, 25% criminal, with the felony backstop

New York is one of the strictest cap states in the country. Under New York General Obligations Law 5-501, the civil usury cap is 16%. Under New York Penal Law 190.40, charging interest above 25% on most consumer loans is a Class E felony, punishable by up to four years in prison.

Two carveouts to know. Loans of $250,000 to $2,500,000 to individuals are subject only to the 25% criminal cap, not the 16% civil cap. Loans above $2,500,000 are exempt from both. For an everyday personal loan of $5,000 to $50,000, the practical ceiling in New York is 16% civil for state-chartered loans and 25% criminal for any consumer loan.

That is why a New York borrower with mid-600s credit often sees a tighter band of offers than a borrower in a permissive state. Lenders that would otherwise quote a 660-FICO file at 28% to 32% in Texas have to either decline the New York applicant, route the file through a federally chartered bank partner, or operate at a loss. Most decline.

Texas: 10% constitutional default plus OCCC quarterly ceilings

Texas operates on a different architecture entirely. Article 16, Section 11 of the Texas Constitution sets a default 10% maximum interest rate absent statutory authority. The Texas Office of Consumer Credit Commissioner (OCCC) publishes quarterly rate ceilings under Texas Finance Code sections 303.003, 303.009, and 304.003. CPI-adjusted brackets are published annually in the Texas Credit Letter and take effect July 1.

The practical effect: licensed Texas lenders operate under multiple statutory rate ceilings depending on loan size and lender type, layered above the 10% constitutional default. For a typical $5,000 to $25,000 personal loan in Texas, ceilings allow APRs in the high 20s to mid 30s, well above New York's binding limits. Texas is not the most permissive state in the country, but it is meaningfully more permissive than New York for everyday personal loan sizes.

Colorado in 2024 to 2025: the 36% cap and the DIDMCA opt-out fight

Colorado caps consumer loans of $1,000 or less at 36% APR under the Uniform Consumer Credit Code, with stepped-down caps on larger balances. In June 2023, Colorado passed HB23-1229 to opt out of DIDMCA Section 521 preemption, effective July 1, 2024. Several state-chartered banks based in other states sued, arguing the opt-out did not apply to their loans into Colorado.

The 10th Circuit ruled in November 2025 that Colorado's opt-out does apply to out-of-state state-chartered banks lending into the state. The ruling tightened the cap's reach. National lenders that were quoting Colorado borrowers above 36% had to recalibrate. Fintechs that partnered with state-chartered banks to import home-state rates lost that lever inside Colorado, at least within the 10th Circuit.

The strict-cap club

The states that bind hardest on personal loan APRs include New York, New Jersey, Connecticut, Massachusetts, Arkansas, and the District of Columbia. The National Consumer Law Center 50-state survey shows 45 states plus DC cap a $500, 6-month loan; 43 plus DC cap a $2,000, 2-year loan; and 42 plus DC cap a $10,000, 5-year loan. The variance is across loan size: a state may cap small-dollar lending at 36% while permitting much higher rates on larger installment loans.

Arkansas is worth singling out. The state constitution caps consumer interest at the federal discount rate plus 5%, one of the lowest effective ceilings in the country. The result is a small lender footprint and aggressive enforcement of the cap by the state attorney general.

The effectively-uncapped club

Several states permit installment-lending APRs that would be felonies in New York. Mississippi's Credit Availability Act allows APRs above 300% on installment loans up to $3,250, with the sunset extended to July 1, 2030 by 2025 legislation. Utah, Idaho, Wisconsin, and Missouri have similarly permissive regimes for certain product structures.

Florida (2023) raised its top consumer rate from 30% to 36% and extended that ceiling to larger loans. Tennessee similarly raised its maximum interest from 30% to 36% on loans of $100 or more. Both moves were technically tightenings on certain product types and looserings on others, depending on who tells the story. NCLC's annual "Predatory Installment Lending in the States" report is the live reference for this; legislative sessions move these numbers more often than borrowers realize.

What changes when you move

Three different scenarios produce three different answers.

- You have an existing personal loan and you move. Your loan terms stay the same. The contract was governed by the law of the state where it originated. Moving from Colorado to Wyoming does not raise your APR.

- You apply for a new loan after moving. The law of your new state of residence governs the new application. Moving from New York to Texas can open you to lenders that did not quote you before.

- You refinance. A refinance is a new loan, governed by the law of your current state. A New York borrower refinancing a 28% loan they took in Texas before moving will see the New York ceiling apply to the new note.

The Military Lending Act 36% floor

For active-duty servicemembers and their dependents, 10 USC 987 caps total APR (MAPR) at 36% on most consumer credit, including personal loans, credit card debt, and payday-type products. This is a federal floor, not a state ceiling. It binds in every state. A Mississippi storefront installment lender that legally quotes 297% APR to a civilian cannot quote that to an active-duty servicemember. The MAPR includes interest plus fees plus credit insurance plus most ancillary charges, which is a stricter calculation than TILA APR.

How to read your state's ceiling against a lender's offer

Three steps work for any application.

- Find your state's current cap on the National Consumer Law Center's installment-loan APR cap fact sheet. NCLC publishes this annually and updates after each legislative session.

- Compare the lender's quoted APR to your state's binding cap (civil for most loans, criminal for the felony backstop in cap states). If you are unsure how to read what you are looking at, a walk-through of the standard TILA disclosure box will help.

- If the quote exceeds the state civil cap, check whether the lender is operating through a federally chartered bank partner or a state-chartered bank exporting another state's rates under DIDMCA. The disclosure at the bottom of the offer typically names the issuing bank.

If you live in a state that has opted out of DIDMCA preemption (Iowa, Puerto Rico, Colorado), the importing-rates loophole is mostly closed. If you live in a state that has not opted out, expect to see offers above your state civil cap from out-of-state bank-partnered fintechs. Whether those offers are enforceable in your state is a question the courts continue to litigate.

Why this matters for your borrowing decision

Most borrowers shop personal loans without ever checking their state's cap, then wonder why offers vary so much from headlines they read in national publications. Bankrate's average personal loan APR data is an average across 50 different ceilings. Your offer is not an average. It is the lender's risk view of your file pressed against your state's legal ceiling. If you live in New York and you are seeing offers at 14% to 18%, that is the system working. If you live in Mississippi and you are seeing storefront offers at 200%-plus APR, that is also the system working, just with the cap dialed differently. If a Mississippi-style offer is the only thing you can get, the better next move is usually to fix the file before applying again rather than accept it: a few specific credit-score moves in the right window can shift the offers you see.

This is not legal advice. For an active dispute or a loan you suspect violates your state's cap, contact your state attorney general's consumer protection office or a consumer-law attorney. Rates and statutes change with each legislative session.

Frequently Asked Questions

Is there a federal cap on personal loan interest rates?

For most borrowers, no. The Military Lending Act caps total APR at 36% for active-duty servicemembers and dependents. Outside that, state law sets the ceiling. Several attempts to enact a national 36% cap on consumer loans have not become law as of mid-2026.

What is New York's maximum legal interest rate on a personal loan?

16% civil under General Obligations Law 5-501 for most consumer loans, with a 25% criminal usury cap under Penal Law 190.40. Loans above 25% interest are a Class E felony in New York. Carveouts exist for loans of $250,000 and above to individuals.

Why can a Mississippi lender legally charge 300% APR?

Mississippi's Credit Availability Act, with its sunset extended to July 1, 2030, permits APRs above 300% on installment loans of up to $3,250. The state has not adopted a 36% small-loan cap. The legality is statutory, not federal.

Did Colorado's rate cap actually apply to fintech lenders?

The 10th Circuit ruled in November 2025 that Colorado's 36% cap applies to out-of-state state-chartered banks lending into Colorado, following the state's 2024 DIDMCA opt-out. The ruling is binding in the 10th Circuit. Other circuits have not adopted identical reasoning.

Does my state's rate cap protect me if I borrow online?

It depends. If the lender is licensed in your state, the state cap binds. If the lender operates through a federally chartered bank or an out-of-state state-chartered bank under DIDMCA, federal preemption may apply, and the state cap may not. The Madden line of cases and ongoing litigation continue to shape this question.

What is the Military Lending Act APR cap?

10 USC 987 caps total Military Annual Percentage Rate (MAPR) at 36% on most consumer credit for active-duty servicemembers and dependents. MAPR is a stricter calculation than TILA APR because it includes most fees and ancillary charges. The cap binds in every state.