A reader emailed me last spring with a screenshot. She had applied for a $10,000 personal loan, signed inside an e-signature envelope, and watched $9,200 land in her checking account two days later. Her first question: "Where did the other $800 go?" Her second: "Was that legal?"

The answer to the first question was sitting in a one-page form she had clicked past on the way to signing. The answer to the second was yes, because her lender disclosed every dollar of it in the place federal law says it has to: the boxed Truth in Lending disclosure. She just hadn't read it. Most borrowers don't, and that is exactly what this piece is about.

Why this one-page form matters more than the marketing page

The marketing page sells. The pre-qualification screen estimates. The boxed disclosure is the one document where federal law dictates what the lender must show, in what order, and how prominently. It is the single most reliable, federally standardized piece of paper in the entire loan flow.

The rules live in Regulation Z, the implementing rule for the Truth in Lending Act. Reg Z applies to consumer credit transactions of $73,400 or less in 2026, a threshold the CFPB and Federal Reserve raised from $71,900 last year based on a 2.1% CPI-W adjustment. That ceiling covers essentially the entire personal loan market.

Inside Reg Z, two sections do most of the work. Section 1026.17 sets the general rules: disclosures must be clear, conspicuous, in writing, and provided in a form you can keep, before you consummate the loan. Section 1026.18, codified at 12 CFR 1026.18 on Cornell LII, lists the 19 specific items the lender must disclose for a closed-end loan. Five of those items are usually grouped into what compliance officers call "the federal box." Those five are the ones a regulator opens the file and looks at first. They should be the ones you look at first too.

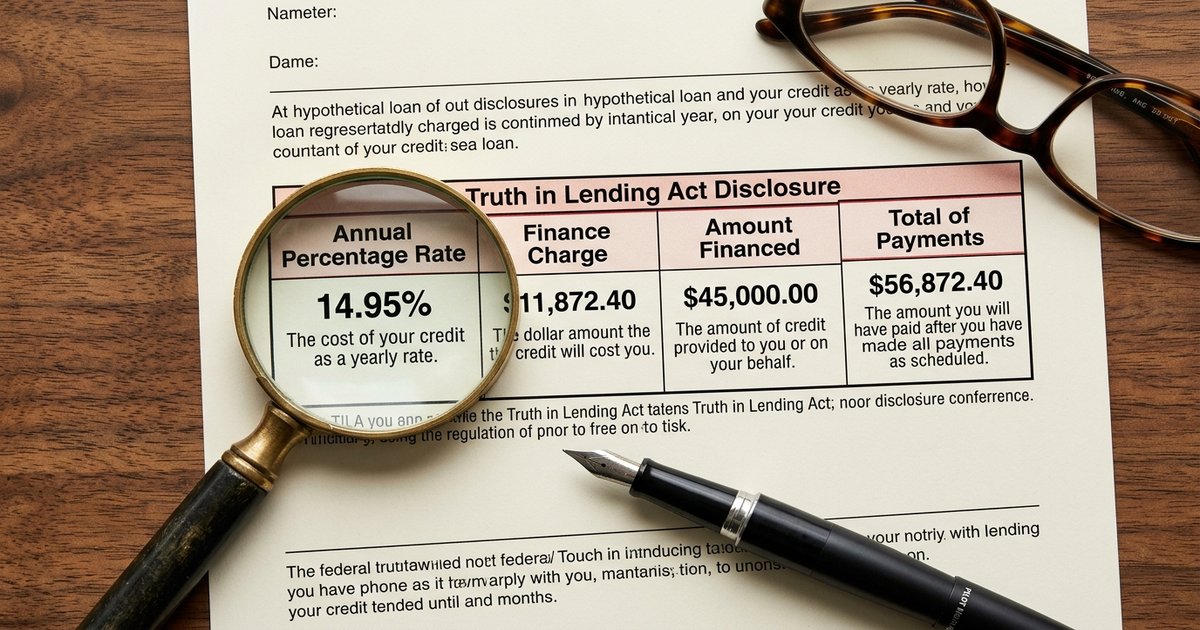

The five numbers in the federal box

Amount Financed: the cash you actually get

Under 1026.18(b), the Amount Financed is the net amount of credit extended on your behalf. Translation: this is what you walk away with after the lender deducts any prepaid finance charge, including the origination fee. If you applied for $10,000 and the lender takes an 8% origination fee, the Amount Financed reads $9,200, not $10,000.

That is the line my reader missed. It is also the most common surprise on r/personalfinance and in Trustpilot reviews of major fintech lenders. Our piece on the hidden origination fee math walks through why a lower headline rate plus a fee can cost more than a higher rate with no fee. The disclosure box is doing its job. The borrower just has to look.

Finance Charge: every dollar above the principal

Reg Z 1026.18(d) requires the Finance Charge to be expressed as a dollar amount, with a mandatory descriptor: "the dollar amount the credit will cost you." That descriptor is not decorative. It is the law. If a disclosure does not say those words, the form is non-compliant.

The Finance Charge bundles the interest you will pay over the life of the loan plus any other charge that meets the regulatory definition of a finance charge. On a 36-month, $10,000 loan at a 14% APR, that number lands somewhere around $2,300 to $2,600 depending on origination fee treatment. On a 60-month loan at 22%, you can clear $6,000 in finance charges on the same principal.

Annual Percentage Rate: the cost of credit as a yearly rate

Section 1026.18(e) gives the APR its mandatory descriptor: "the cost of your credit as a yearly rate." Section 1026.17(a)(2) goes further: the Finance Charge and APR disclosures must be "more conspicuous than any other disclosure" on the form. Bigger type, bolder, set apart. If they aren't, that is itself a TILA defect.

The disclosed APR at consummation is the binding number. The rate the marketing page quoted, the rate the prequalification soft pull suggested, even the rate a loan officer mentioned on the phone, none of those are TILA-regulated. The APR in the box is.

Total of Payments: what you will actually write checks for

Total of Payments is the sum of every scheduled payment, principal and interest combined, over the full term. Borrowers see this number and react: "I am paying back $14,000 on a $10,000 loan?" Yes. That is the math of any closed-end installment credit. The disclosure box is the moment that math becomes legible. Our piece on five personal loan numbers that decide whether a loan is worth taking uses this number as the primary comparison.

Payment Schedule: how many, how much, when

The schedule lists number of payments, amount of each, and timing. On most personal loans you get a fixed monthly payment for 24, 36, 48, or 60 months. Anything else (a balloon at the end, a step-up payment, an interest-only period) has to appear here. If you see a payment line that does not match what you were told verbally, stop signing.

The three numbers a regulator checks first

If a CFPB examiner pulls a personal loan file under the agency's TILA examination procedures, the first move is to verify three numbers reconcile.

One: Amount Financed should equal the loan amount the borrower agreed to, minus any prepaid finance charge that was disclosed. Two: Total of Payments should equal the sum of the scheduled payments, exactly. Three: APR should be calculable from Amount Financed, Finance Charge, and the payment schedule using the actuarial method in Reg Z Appendix J.

You don't need to run Appendix J yourself. You need to do the cheap version: confirm the Amount Financed equals what the lender promised to deposit, multiply the monthly payment by the number of payments, and compare to the Total of Payments line. They should match within rounding. When they don't, you have either a math error or a charge you weren't told about.

A worked example: $10,000 advertised, what the box really says

Say you applied for a $10,000 unsecured personal loan, 36 months, at a quoted 13.99% APR with an 8% origination fee. Here is what the federal box should look like:

- Annual Percentage Rate: roughly 19.0% (the origination fee gets folded in, which is why APR is higher than the quoted interest rate)

- Finance Charge: roughly $2,400

- Amount Financed: $9,200 (the $10,000 less the $800 origination fee)

- Total of Payments: roughly $11,600

- Payment Schedule: 36 monthly payments of approximately $322

Three things to notice. The APR is meaningfully higher than the interest rate, because origination fees are baked into APR by design (that is the entire point of Reg Z's APR calculation). The Amount Financed is not the loan amount you applied for. And the Total of Payments minus the Amount Financed should approximately equal the Finance Charge: $11,600 minus $9,200 is $2,400. If those numbers don't reconcile in your box, something is wrong.

Five red flags hiding in plain sight

Even on a fully compliant disclosure, there are clauses that quietly change the deal. Look for these.

1. Prepayment penalty language. Reg Z 1026.18(k) requires a statement of whether a penalty applies if you pay the loan off early. Most reputable personal lenders waive prepayment penalties; some do not. The box will tell you, but only if you read the prepayment line.

2. Security interest on a loan you thought was unsecured. Section 1026.18(m) requires disclosure of any security interest. If your "unsecured" personal loan lists a security interest in a vehicle or deposit account, it isn't unsecured.

3. Late charge math. Section 1026.18(l) requires disclosure of late charges. Some lenders charge a flat $15 to $39; others charge a percentage of the past-due payment. A 5% late fee on a $400 monthly payment is $20 once. Over a year of stumbles, that adds up.

4. Balloon payment schedules. If the payment schedule shows 35 equal payments and one big final payment, that is a balloon, and it is legal but rare on personal loans. Make sure you intended that structure.

5. Missing itemization of Amount Financed. Section 1026.18(c) entitles you to an itemization of where the Amount Financed went, on request. If a lender refuses or buries the itemization behind a click-through, that is a Reg Z compliance question worth asking out loud.

What to do if the numbers do not match what you were quoted

Stop signing. The disclosure has to be delivered before consummation under 1026.17(b), which means you have time. Call the lender, point to the specific line, and ask why the number differs from your quote. Get the answer in writing, ideally by email. (If the pitch came in over email or text in the first place and feels off, our piece on how to spot a personal loan scam covers the warning signs.)

If the lender cannot or will not explain, you have options. You can walk away (the prequalification offer is not binding on you). You can file a complaint with the CFPB at consumerfinance.gov/complaint, which generally produces a lender response within 15 days. Material TILA disclosure errors can support a private right of action under 15 USC 1640 for statutory and actual damages, though that route generally requires a consumer-rights attorney.

One myth to put down: TILA does not give you a right to rescind an unsecured personal loan. The rescission right under 15 USC 1635 applies to certain loans secured by your principal dwelling. Once you sign and the funds disburse on a personal loan, you are on the hook unless you can prove the lender violated the rules.

Where TILA stops and ECOA, FCRA take over

The disclosure box governs the loan you got. It does not govern the loan you didn't get. If you were denied, your rights live under the Equal Credit Opportunity Act (Regulation B) and the Fair Credit Reporting Act, which together require an adverse action notice with specific reasons and credit score information. We walk that letter line by line in your rights when a lender denies you.

If you were approved at a worse rate than the lender's best available, you may also receive a risk-based pricing notice under FCRA / Regulation V. Read it. It tells you the lender priced you up because of something on your credit file you can probably do something about.

A short checklist to keep next to the signing screen

- Find the box. It should be set apart, with APR and Finance Charge in larger or bolder type.

- Confirm Amount Financed matches the cash you expect to receive.

- Multiply the monthly payment by the number of payments. Compare to Total of Payments.

- Subtract Amount Financed from Total of Payments. That number should equal the Finance Charge.

- Read the prepayment, late charge, and security interest lines. Out loud, if it helps.

- Save a PDF copy. Reg Z 1026.17 entitles you to a form you can keep. Keep it.

The box looks like boilerplate. It is not. It is the borrower's primary protection, written by federal regulators because they know the rest of the loan flow is designed to move you toward signature. Spend two minutes on it. The borrower who sent me that screenshot now reads the box first, every time. So should you.

Frequently Asked Questions

What is a Truth in Lending disclosure on a personal loan?

It is the federally required, standardized disclosure form that shows your APR, Finance Charge in dollars, Amount Financed, Total of Payments, and payment schedule. Reg Z 1026.18 sets the content. The lender must deliver it before you finalize the loan.

Why is the Amount Financed lower than the loan amount I applied for?

Because the lender deducts any prepaid finance charge, most often the origination fee, before disbursing. If you took a $10,000 loan with an 8% origination fee, your Amount Financed is $9,200 and the $800 fee is bundled into your Finance Charge and APR.

Is the APR in the disclosure box the same as the rate I was quoted?

Not always. The APR at consummation in the box is the binding number under TILA. Marketing rates and prequalification rates are estimates. The box reflects the actual deal you are about to sign.

Can I cancel a personal loan after I sign?

Generally no. The TILA rescission right under 15 USC 1635 applies to certain loans secured by your principal dwelling, not to unsecured personal loans. Some lenders offer a voluntary cooling-off period; check your loan agreement.

What should I do if the disclosure box numbers don't match my quote?

Stop and ask the lender to explain in writing before you sign. If the answer doesn't reconcile, you can walk away or file a complaint with the CFPB. Material disclosure errors can support a private claim under 15 USC 1640.

Does the disclosure cover prepayment penalties?

Yes. Reg Z 1026.18(k) requires the lender to state whether a prepayment penalty applies. Most reputable personal lenders waive it, but read the line before you assume.