You've already been told you'll need a co-signer. Maybe the lender said it outright, maybe you ran the prequalification and the offer came back at a rate you can't stomach. Either way, you're now sitting with a different problem: you have to ask someone you love to put their credit on the line for you, and you don't quite know how.

This isn't a "make sure you trust them" article. You already trust them, that's why they're on your list. What you actually need is the language for the conversation, the numbers you owe them before they sign, and a clear-eyed picture of what happens if life goes sideways and a payment gets missed. Let's go.

What a co-signer is (and is not)

A co-signer is someone who agrees to be equally responsible for a debt without receiving any of the loan proceeds. Their name is on the contract. Their credit is on the line. They get nothing in their pocket.

A co-borrower is different. Co-borrowers share equal liability and equal access to the funds (think of a couple buying a car together). Co-signers have liability without access.

The Federal Trade Commission (FTC) has been blunt about this for decades. Under the FTC Credit Practices Rule (16 CFR 444.3), lenders are required to give co-signers a written notice before they sign that says, in plain language: "You are being asked to guarantee this debt. Think carefully before you do. If the borrower doesn't pay the debt, you will have to. Be sure you can afford to pay if you have to, and that you want to accept this responsibility." Read that notice with your co-signer before either of you signs anything. Out loud, if it helps. It's the most honest sentence in the entire loan packet.

The part most people miss

Here's what surprises borrowers and co-signers alike: the lender doesn't have to chase the primary borrower first. Per the FTC, lenders can demand payment from the co-signer the moment a payment is missed. There's no "I'll wait and see if my kid pays" buffer. Day 31 of a missed payment, the calls start, and they may go to your co-signer first.

Before you ask: the four numbers you owe them

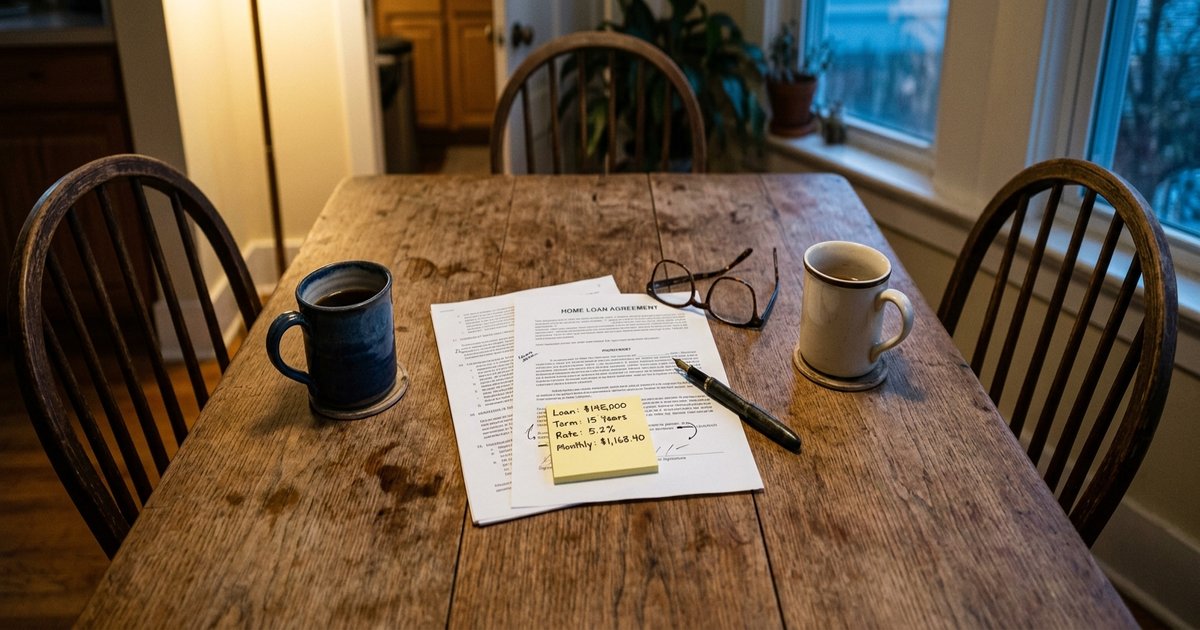

If you're going to ask someone to attach their credit file to your loan, walk in with the actual loan terms in hand. Not "I'm thinking about borrowing some money." The four numbers that need to be on a sticky note before you have the conversation:

- Loan amount (the principal you're borrowing)

- Term (how many months until it's paid off)

- Monthly payment (the dollar amount due every month)

- Total of payments (principal plus all interest over the full term, the number that makes the loan real)

For example: "I'm asking you to co-sign a $10,000 loan, 60-month term, $213 a month, total of payments around $12,800." Now they know exactly what they're guaranteeing. Vagueness here is unfair to them. Our piece on the five personal loan numbers that decide whether a loan is worth taking has the worksheet for pulling those numbers cleanly.

The script: how to ask without asking for a favor

The hardest part of the conversation is your tone, not your words. You're not asking for a gift. You're proposing a serious financial arrangement that has consequences for both of you. Treat it that way and they'll meet you there.

Sample script for asking a parent

"I want to talk to you about something I'm working on, and I want you to feel completely free to say no. I've been quoted a personal loan to (consolidate my credit cards / cover this medical bill / fund this move), and the rate I qualify for on my own would cost me about $3,400 more over the life of the loan than the rate I'd get with a co-signer. The loan would be $10,000, 60 months, $213 a month, total of about $12,800. I'm not asking you to make payments. I'm asking you to be on the contract so I get a fair rate. I want to walk you through what happens if I miss a payment, what your credit exposure looks like, and what we'd put in writing between us before either of us signs anything. Can we sit with this for a week before either of us decides?"

Sample script for asking a sibling

"I need to ask you something, and I need you to take your time with it. I'm trying to get a personal loan, and the bank wants a co-signer. You're the person whose credit could help me, but I also know what I'd be putting on your file. I want you to know what the loan is, what the math looks like if I miss a payment, and how I'd want us to handle that, before you decide. I'm not going to be weird if you say no. I'd rather you say no now than feel trapped later."

Boundary-setting language for the co-signer

If you're the one being asked, here's language that protects both of you. None of this is unreasonable; if any of it is met with pushback, that's information.

- "I want to be added as an authorized contact on the loan so I see statements directly, not through you."

- "I'd like us to set up automatic payments out of an account I can monitor."

- "If you anticipate a missed payment, I want to know two weeks before, not the day of."

- "I want us to put in writing what happens if you can't pay, including whether you'll refinance to remove me as soon as your credit qualifies."

- "I want to read the FTC co-signer notice with you before we sign."

What you should both put in writing (separate from the loan)

This document doesn't change the legal contract with the lender, but it changes the relationship. A simple side agreement between borrower and co-signer should cover:

- Who pays the loan (almost always: the primary borrower, every month, on time)

- How the borrower will notify the co-signer if they're going to be late (and how far in advance)

- What happens if the borrower misses a payment (does the co-signer step in, get repaid later, charge a fee?)

- Whether the borrower commits to refinancing the loan into their name only as soon as they qualify

- What happens to the loan if either party becomes incapacitated or dies

Sign it. Date it. Each keep a copy. Is it a legally binding contract? Probably, depending on your state, but its real purpose is forcing both of you to think through the scenarios before they happen.

What happens at the first missed payment

Whose phone rings first

The lender will call both of you. Sometimes the co-signer first, especially if there's a phone tree where the borrower's number is busy. One borrower described it on Reddit: "The lender called my mom before they called me when I missed a payment. She had no idea she was first in line for collection calls." This is normal. Co-signers receive collection contact under the same Fair Debt Collection Practices Act (FDCPA) rules as primary borrowers.

How fast the credit hit lands

Payments are typically reported as late once they pass 30 days past due. Per myFICO's factor breakdown, payment history accounts for 35% of a FICO score, the largest single factor. A single 30-day late on a co-signed loan can drop a co-signer's score by 60 to 110 points, even if their credit was previously perfect. That late mark stays on their report for seven years from the date of original delinquency under the Fair Credit Reporting Act (FCRA).

Read that again. One missed payment. Seven years on their file. That's the math, and your co-signer deserves to hear it before they sign.

The 30, 60, 90 day collection escalation

Most personal loans follow a pretty consistent escalation pattern:

- Day 1 to 14: Late fees may apply per the loan contract. No credit reporting yet.

- Day 30: The first late payment hits the credit reports of both the borrower and the co-signer.

- Day 60 to 90: Additional late marks. Calls escalate. Some lenders begin internal collections.

- Day 120 to 180: The loan may be charged off and sold to a third-party collection agency. Both borrower and co-signer can be sued.

- Post-judgment: Wage garnishment is possible after a court judgment in most states, capped at 25% of disposable earnings or the amount above 30 times the federal minimum wage, whichever is less (15 U.S.C. 1673).

The CFPB has also documented "auto-default" clauses in some loan contracts that can demand immediate full repayment if the co-signer dies or files bankruptcy, even if the primary borrower is current. Read your contract for this clause. If it's in there and you're uncomfortable, ask the lender to remove it or shop another lender.

How to release a co-signer

This is the conversation that almost nobody has at the start of the loan, and almost everybody wishes they'd had at the end.

The CFPB has reported that 90% of private student loan borrowers who applied for co-signer release were rejected. That's a private student loan figure specifically, not all loans, but the underlying dynamic shows up across most consumer credit: lenders rarely volunteer to drop a guarantor.

That leaves three real paths to release:

- Pay the loan off in full. The cleanest exit. The contract ends, both parties' obligations end.

- Refinance the loan in the borrower's name only. Once the borrower's credit has improved enough to qualify on their own, refinancing replaces the old loan with a new one without the co-signer. This is the path most borrowers actually take. Our piece on three credit score moves that work in 60 days covers the score-lift moves that get you ready to refinance.

- Apply for a contractual co-signer release. Some lenders offer a release after a certain number of consecutive on-time payments (often 12 to 36) and a credit re-evaluation of the primary borrower. Most personal loan contracts don't include this; check yours.

If the loan is paid off via refinance or payoff, ask the lender for a written confirmation that the original account is closed and the co-signer is released. Save that letter.

When co-signing is the wrong answer

Sometimes the right move is not to take the loan with a co-signer, but to take a different product or wait. A few alternatives worth weighing:

- A secured credit card. You put down a deposit (typically $200 to $500), use the card normally, and your on-time payments build credit.

- A credit-builder loan. A small loan from a credit union where the funds sit in a savings account while you make payments.

- A smaller unsecured loan you qualify for alone. Sometimes the right move is to borrow less, on worse terms, and protect the relationship.

- Waiting six months. If the loan isn't urgent and your credit is improving, six months of on-time payments on existing accounts can move your score enough to change your offers materially. Our piece on what a 580 FICO actually costs vs a 680 shows the dollar value of waiting.

Trust Point Loans isn't a lender, and we're not in a position to tell you whether co-signing is right for your specific family. What we can tell you is that the FTC, the CFPB, and a long stretch of borrower forums all point to the same lesson: the conversation before signing matters more than any clause in the contract. Have the conversation. Have it twice if you need to. And read the FTC notice together before either of you puts a pen down.

Frequently Asked Questions

Does co-signing show up on the co-signer's credit report?

Yes. The loan appears on the co-signer's credit report as if it were their own debt, including the balance and payment history. This affects their debt-to-income ratio and can make qualifying for their own future loans harder.

Can I be removed as a co-signer after the loan is in good standing?

Sometimes, but rarely automatically. Most personal loan contracts don't include a co-signer release clause. Your real options are usually: have the primary borrower refinance into their own name, pay the loan off, or apply formally for release using a template letter (the CFPB publishes one).

What's the difference between a co-signer and a co-borrower?

A co-signer guarantees the debt without receiving any of the loan funds. A co-borrower has equal access to the funds and equal liability. Both share equal credit-reporting consequences, but only the co-borrower benefits from the loan proceeds.

How much can a missed payment hurt a co-signer's credit?

A single 30-day late payment can drop a co-signer's score by 60 to 110 points if their credit was previously clean, since payment history is 35% of a FICO score. The late mark stays on their credit report for seven years under federal law.

Can a lender go after the co-signer before the primary borrower?

Yes, in most cases. The FTC's co-signer notice specifically warns that lenders can demand payment from the co-signer the moment a payment is missed. They aren't required to exhaust collection efforts against the primary borrower first.

What happens to a co-signed loan if the co-signer dies?

It depends on the loan contract. Some contracts include "auto-default" clauses (documented by the CFPB) that demand immediate full repayment if the co-signer dies or files for bankruptcy, even if the primary borrower is current. Read the contract before you sign.