This story is a composite. It is not the story of one named individual. The numbers, the timing, and the behavioral checkpoints are drawn from typical patterns in the CFPB Consumer Complaint Database, Federal Reserve consumer-finance research, NBER behavioral-finance studies, and current 2026 lender disclosures. I assembled it because I have walked dozens of borrowers through versions of this same plan, and the pattern that works looks roughly like this. Your numbers will differ. The framework will not.

The kitchen table moment

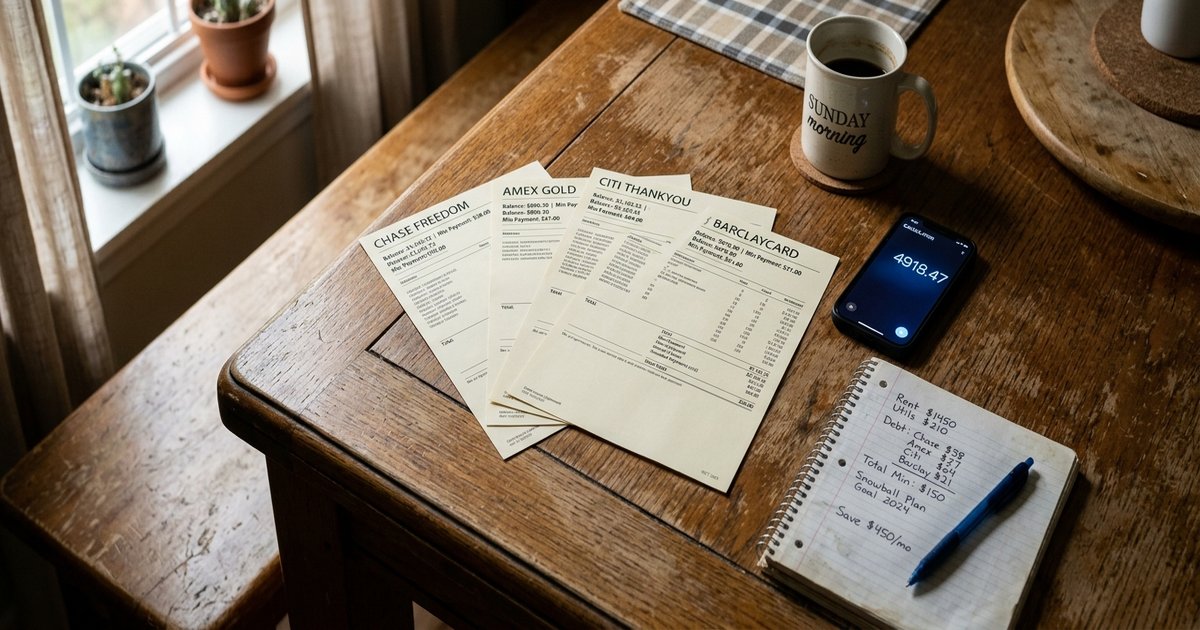

Picture an ICU nurse in her mid-thirties. $74,000 W-2 income. Renting. 685 FICO. Four credit cards. Total revolving balance: $24,000.

It is a Sunday in February. She has all four statements spread on the kitchen table because the balances stopped going down a year ago and she finally wants to know why. She does the math with a calculator on her phone.

Minimum payments across the four cards add up to about $620 a month. At a blended APR of 22% (the national average card APR has run well above 20% since 2024 according to the Federal Reserve's G.19 Consumer Credit data), interest is eating roughly $440 of that $620 every month. So $620 leaves the account, $180 of it touches principal, and $440 funds someone else's quarterly earnings call.

That is the moment. Not panic. Just the math becoming undeniable.

Why she did not pick the obvious paths

Two options came up first because they always come up first.

Balance transfer card. Her FICO was good enough to qualify, but the strongest 0% promotional periods cap at 21 months. $24,000 over 21 months is roughly $1,143 a month in principal alone, before counting the 5% transfer fee that adds $1,200 to the balance on Day 1. She could not sustain $1,200 a month against rent, groceries, student loan payments, and a car. The structure would collapse around month 9 and the retroactive interest rules on some cards would catch the full balance at the back end.

HELOC. She was renting. No equity, no path. (For homeowners, the HELOC math at 2026 rates can be the cheapest option in this article. For renters, it is not on the table. Our piece on debt consolidation without a personal loan walks the four alternatives in detail.)

401(k) loan. She had a balance but the ICU staffing shake-ups in her hospital system that year made job stability feel less than airtight. A 401(k) loan that accelerates if you separate from the employer, becomes a deemed distribution if unpaid, and triggers ordinary income tax plus a 10% penalty if you are under 59 and a half? She read the IRS page once and decided no.

That left an unsecured personal loan.

What the lender shopping actually looked like

She prequalified at three lenders. All soft pulls, no score impact. The offers came back inside an hour. (Why the same file gets such different quotes is its own story; we cover it in why two lenders quote you wildly different APRs on the same day.)

- Lender A: 13.49% APR, 5% origination fee, 60-month term.

- Lender B: 14.49% APR, 3% origination fee, 60-month term.

- Lender C: 12.99% APR, 7% origination fee, 60-month term.

The obvious move would be to chase the lowest sticker rate (Lender C at 12.99%). The TILA-required disclosure box (12 CFR 1026.18) tells a different story. The origination fee comes off the Amount Financed before the cash hits her account. So:

- Lender C nets her $22,320 on a $24,000 gross loan, but she pays interest on the full $24,000.

- Lender A nets her $22,800 on the same gross.

- Lender B nets her $23,280 on the same gross.

Once she ran the total of payments numbers from each disclosure box, Lender B (14.49% APR, 3% origination) came out as the cheapest total cost over 60 months despite not having the lowest sticker APR. The lesson, the one I have repeated in front of borrowers more times than I can count: read the disclosure box, not the marketing page. (The full version of this lesson lives in our piece on the hidden origination fee math.)

The 28-month plan

She accepted Lender B. Because the loan amount needed to net at least $24,000 in cash to clear the cards, she sized the loan to gross $24,743, which after the 3% origination ($742) deposited $24,001 in her account. She paid all four cards in full the same week the funds landed.

The contractual scheduled payment on a $24,743 loan at 14.49% over 60 months is approximately $581 per month. Total of payments at the scheduled rate would be roughly $34,860, with about $10,117 in interest paid over five years.

That is where most "consolidation" stories stop. They take the relief, ride the schedule, and end up paying the full $10,000 in interest. She ran a different play.

She added $325 a month to every payment. $581 + $325 = $906 monthly. That extra $325 went straight to principal. At that rate, the loan retired in roughly 28 months instead of 60, and total interest dropped to under $4,800. She saved roughly $5,300 in interest over the life of the loan by making the prepayment a habit.

Where did the $325 come from? Three places, all unglamorous:

- The minimum payments she used to send to the four cards ($620) now had no destination. She redirected $325 of that to extra loan principal and let the rest absorb into household cash flow.

- She paused two streaming services and a meal delivery subscription. About $80 a month.

- She picked up one extra ICU shift per month, net pay roughly $400 after taxes.

The redirected card minimums are the key insight. Most consolidation borrowers feel the relief of one payment instead of four and quietly let the difference disappear into lifestyle. The plan only works if the freed-up cash gets a job.

The rules she set in writing

The behavioral failure mode in consolidation is not the math. It is the cards refilling while you pay down the loan. So the rules went on a sticky note on the fridge:

- The cards stay open. Closing them would shorten her average account age and shrink her total available credit, both of which would tank her FICO right when she needed it most.

- The cards stay at zero. No grocery runs, no "I will just put the gas on it this week."

- One card runs a $9 streaming charge on autopay, paid off automatically each month, so the issuer does not close the account for inactivity.

- Emergency fund first. She built a $1,000 starter emergency fund in the first six weeks before adding the prepayment to the loan. By month nine she had it to $2,500.

Avalanche or snowball: she used both

The behavioral-finance debate is not academic. NBER Working Paper 24161 (Gal and McShane) found that borrowers using the snowball method (smallest balance first, regardless of rate) had higher follow-through and were more likely to eliminate their debt entirely, even though the avalanche method (highest rate first) minimizes total interest paid mathematically.

She did not pick one. The consolidation itself was the avalanche move, replacing 22% blended card APR with 14.49% loan APR. The remaining behavior, the prepayment, was snowball-flavored: every time the principal hit a round number ($20,000, then $15,000, then $10,000), she let herself stop and notice. The visible progress is what kept her on the plan when nothing else did.

Month 11: the car repair

Of course there was a car repair. There always is. $1,400 transmission work in month 11. This is the moment the typical consolidation story goes off the rails: borrower charges the repair to a card, balance starts climbing again, the loan is now stacked on top of fresh card debt.

She used the emergency fund. $1,400 came out of the $2,500 she had built. The cards stayed at zero. The loan prepayment held that month. She rebuilt the emergency fund over the next four months by temporarily reducing the prepayment from $325 to $200, then back to $325 once the buffer was rebuilt.

That is the entire emergency-fund argument distilled to one paragraph. The fund is not for retirement. It is the firewall that stops a consolidation plan from collapsing on first contact with reality.

Month 18: the raise and the temptation

She got a $4,800 annual raise. Net of taxes, about $300 a month.

The temptation is to absorb the raise into lifestyle (you earned it, after all). The plan said otherwise. She added $250 of the $300 to the loan prepayment, bringing total monthly payment to $1,156. The remaining $50 went into the emergency fund until it hit $4,000, at which point that excess shifted to the loan as well.

Compounding cuts in both directions. She cut the remaining loan term by another four months by directing the raise to debt instead of dinners.

Month 28: payoff

Final payment cleared in month 28. The four cards still sat at zero. The emergency fund was at $4,000. FICO had drifted from 685 to 742, mostly because revolving utilization went from above 70% on most of the cards to under 5% the day the consolidation funded, then stayed there. Length of credit history kept growing because the cards stayed open.

Three habits stayed after the loan retired:

- The $906 a month she had been sending to debt rerouted: $200 to the emergency fund (now targeted at six months of expenses), $500 to a Roth IRA, $206 to a sinking fund for the next car.

- The cards stayed in a drawer. One kept its $9 streaming charge running.

- She kept reading her statements every month, not because she was nervous, but because that is the habit that started the whole thing.

What this story does not promise

This composite was built to show one realistic path, not a guarantee. The plan does not work cleanly for:

- Borrowers below 640 FICO. The personal loan APRs available below 640 in 2026 routinely run 25% to 35.99%. The spread that makes consolidation worthwhile shrinks or disappears. The DMP path through a nonprofit credit counselor is the more realistic option in that tier.

- Borrowers without stable income. A consolidation loan without a steady paycheck just transfers the cliff from "carrying card balances" to "missing loan payments and getting a 30-day late on the credit file." That is worse, not better.

- Borrowers whose DTI already exceeds 50%. Most personal loan lenders cap accepted DTI at 50%. If you are already there, you will not get the loan, or you will get it at a rate that defeats the purpose.

- Anyone who cannot commit to keeping the cards at zero. The single most common failure mode is "consolidate, then refill the cards within a year." Now you are servicing the loan plus fresh card balances. The plan needs the behavioral rule, not just the financial math.

The five numbers any reader should pull before doing the same math

If you are sitting at your own kitchen table this Sunday wondering whether some version of this works for you, here is what to write down before you do anything else (our piece on the five personal loan numbers that decide whether a loan is worth taking walks each one in detail):

- Your blended card APR. Not the worst card. The weighted average across all your balances.

- Your total monthly minimum payments today. This is your baseline cash flow.

- Your gross monthly income and your DTI. Underwriters cap most personal loans at 50% DTI, prefer below 36%.

- Your FICO score from the bureau the lender will pull. Most personal lenders pull FICO 8 or 9, not VantageScore. The score in your banking app may not be the one the lender sees.

- The actual disclosure box from at least three prequalification offers. APR, origination fee, total of payments. The TILA box, not the marketing page.

Those five numbers tell you whether your version of this plan is realistic, marginal, or wrong for your situation. They take 30 minutes to gather. They are worth more than any article on this site.

Trust Point Loans is not a lender. We publish composite case studies like this one because the math is more honest when it is grounded in real numbers, real lender disclosures, and behavioral research instead of marketing copy.

Frequently Asked Questions

Is a 28-month payoff realistic for $24,000 of card debt?

It is realistic for a borrower with stable income, a 14% to 15% personal loan APR, and the ability to add roughly $325 per month above the scheduled payment. Different income levels and APRs produce different timelines.

Why did the lower-APR loan offer in this story turn out to be more expensive?

Because origination fees come out of the Amount Financed before the cash hits your account, but you pay interest on the full gross loan. A 12.99% APR with a 7% origination fee can produce a higher total cost than a 14.49% APR with a 3% origination fee on the same gross amount.

Should I close my credit cards after consolidating?

For most borrowers, no. Closing cards shrinks total available credit and shortens average account age, both of which can drop your FICO by 20 to 40 points right when you wanted the score to improve. Keep the cards open at zero balances.

What if I cannot afford the extra prepayment?

The plan still works on the scheduled payment, just slower and with more interest paid over the full term. A 60-month payoff at 14.49% on $24,000 leaves you debt-free in five years instead of 28 months. That is still better than the trajectory of card minimums at 22% indefinitely.

Can I consolidate with bad credit?

Below 640 FICO, personal loan APRs in 2026 routinely run 25% to 35.99%, which often defeats the purpose of consolidating from cards in the low 20s. Better paths in that credit tier include a nonprofit Debt Management Plan through NFCC.org or FCAA.org.

Why use the snowball method if avalanche saves more interest?

NBER Working Paper 24161 found that borrowers using snowball-style approaches (smallest balance first or visible-progress milestones) followed through more reliably than borrowers using strict avalanche. Total dollars matter, but completion matters more.