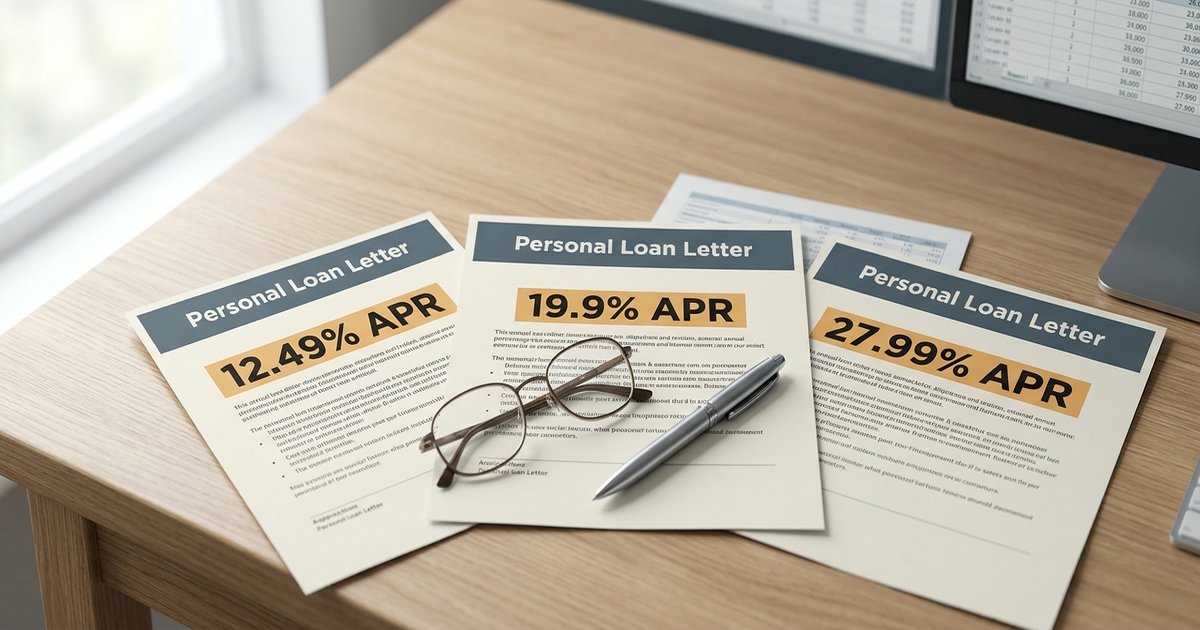

A 44-year-old homeowner in suburban Atlanta prequalified at three personal loan lenders on the same Tuesday morning in April. Same income on file, same 712 FICO, same $25,000 request, same 60-month term. The first quote came back at 12.49% APR. The second at 19.9%. The third at 27.99%. Fifteen and a half percentage points of spread on identical inputs. Over the life of the loan, the gap between the cheapest and most expensive offer was just over $11,800 in interest.

That kind of variance is not a glitch. It is the system working as designed. Once you understand the inputs each lender weighs differently, the spread stops looking arbitrary and starts looking like five or six separate pricing decisions stacked on top of one another.

The same applicant, three different APRs

Start with what is actually identical between offers and what is not. Identical: the borrower's credit file, income, requested amount, and term. Not identical: each lender's internal risk model, its cost of funds, how it interpreted the loan purpose field, the pricing tier the algorithm dropped the file into, and the relationship discounts attached to the quote.

The Federal Reserve's September 2025 FEDS Note on consumer loan pricing put the relationship plainly: expected loss and origination pricing move together across lenders, but each lender's internal estimate of expected loss is its own model, trained on its own book. SoFi's view of a 712 FICO with a $90,000 income is not the same as Best Egg's view of the same borrower, because the two have lent to different people and watched those people repay (or not) over different windows of time.

SoFi's own consumer-facing explainer concedes the spread between best and worst APR for the same loan amount across lenders can exceed 12 percentage points. Real-world spreads in 2026 sometimes run higher.

Five things lenders price on that have to do with you

Your credit data, but not the way you think

FICO is the input most borrowers fixate on. It is also the input most lenders agree on. Where the agreement ends is everything else in your credit file: utilization on revolving accounts, recent inquiries, the age of your oldest tradeline, the presence of any installment loan paid to term, and whether you have ever carried a balance through a hardship period. Two lenders looking at the same 712 FICO can read a thin file (three accounts, all under five years old) very differently from a deep file (eleven accounts, oldest opened in 2008, perfect payment history).

One lender weights utilization heavily. Another weights tradeline age. The CFPB confirms this is what risk-based pricing actually means under FCRA: lenders are allowed to charge different APRs based on credit risk inputs, and they are allowed to weight those inputs however their model performs best on their book. If the file has thin spots you can address, our piece on three credit score moves that work in 60 days goes through the moves that actually shift a model's read.

Your debt-to-income ratio

DTI is where two applicants with identical FICOs can split sharply. A borrower carrying $1,800 in monthly debt service on $7,500 of gross income is in a different bucket than one carrying $400 on the same income. Most fintech lenders have hard DTI ceilings between 40% and 50%, and pricing tiers below those ceilings step up by a few points each.

Loan purpose

This one surprises borrowers. Lenders ask why you want the money, and the answer is a pricing input. Credible's APR trend data shows debt consolidation loans price below "other" purposes at the same lender, because credit card refinance applicants have, in lender data, repaid more reliably than people borrowing for travel or a major purchase. Be honest. Lying on a loan application is fraud, and you do not need to game it: the difference between consolidation and "major purchase" at most lenders is one to three points, not ten.

Loan term and amount

A 36-month loan typically prices below a 60-month loan at the same lender, because the lender's exposure to default risk grows with time. Smaller loans sometimes carry higher APRs because fixed origination costs are spread across less principal. The first-time borrower who asks for $40,000 over 84 months should not be surprised when that quote comes in higher than $20,000 over 36.

Autopay, direct deposit, and relationship discounts

Most major lenders attach a 0.25% to 0.50% APR discount to autopay. SoFi adds another small discount for direct deposit into a SoFi account. Discover and credit unions often quote a "member" rate that is materially below the screened rate. These are real, but they are also why the rate on the marketing page is rarely the rate you get without doing something extra.

Five things lenders price on that have nothing to do with you

The lender's cost of funds

A bank-owned lender (Discover, Marcus when it was active, most credit unions) funds loans from deposits. Deposit costs in 2026 are higher than they were in 2021 but lower than peak 2024. A marketplace lender (Upstart, Prosper, LendingClub) funds through capital markets and institutional buyers, and that funding costs more. The wholesale cost difference flows directly into the APR you see. Two lenders with identical risk views of your file can still price five points apart because their cost of capital is five points apart.

The lender's target risk tier

LightStream's published starting APR in May 2026 was 6.49%. Best Egg's was 7.99%. Upstart's was 7.80%. SoFi's was 8.99%. Those numbers signal who each lender is trying to attract. LightStream wants the 780-FICO homeowner with a deep file. Upstart's algorithm was originally built to approve thinner files at reasonable rates by reading variables FICO ignores. A 712 borrower walking into LightStream is below that lender's prime tier and gets priced accordingly. The same borrower at Upstart sits squarely in the model's sweet spot.

How the model treats thin-file vs deep-file applicants

Algorithmic underwriting decides a large share of personal loan applications at fintech lenders without a human ever touching the file. Upstart's own SEC filings detail the role of its proprietary model. A model trained on younger borrowers with thinner files will price a 28-year-old graduate student more aggressively than a model trained on a book of 50-year-old prime borrowers. Same FICO, different model, different rate.

State rate caps

Federally chartered credit unions cap personal loan APRs at 18% under NCUA rule, regardless of what their model would otherwise produce. Several states impose lower civil usury caps on certain loan sizes. A New York borrower and a Texas borrower can see different ceilings on the same lender's offer because state law sits on top of the model output. We cover the state map in a separate piece on state rate caps.

Marketing posture

Some lenders run loss-leader pricing on their advertised starting rate to win the click, then price most actual borrowers higher. Others price closer to the middle of their book and accept fewer top-of-funnel leads. The starting APR on a landing page tells you what the lender will quote its best applicant. It tells you almost nothing about what they will quote you.

How to read three offers without getting fooled by the headline rate

When you have three quotes, the comparison should run on four lines, not one.

- APR, not interest rate. APR includes origination fees under TILA. Interest rate does not. A 9.99% interest rate with a 6% origination fee is not a 9.99% loan. The mechanics are walked through in our breakdown of origination fee math.

- Total of payments. Multiply the monthly payment by the number of months. This is the actual dollar cost.

- Amount financed. The TILA disclosure box tells you what you actually receive after fees. If a lender deducts $1,500 in origination from a $25,000 loan, your amount financed is $23,500, not $25,000.

- Discounts already applied? Confirm whether the quoted APR assumes autopay or relationship discount. Sometimes it does, sometimes it does not.

When the high quote is correct

Sometimes the 27.99% offer is not a lender being uncompetitive. It is a lender being honest about what its model thinks of the file. If the borrower has a recent charge-off, an open collection, or a thin file with no installment history, a 12.49% offer from a competing lender may be a teaser the borrower will not actually qualify for at the hard-pull stage. Better to confirm the conditional offer holds through full underwriting before walking away from the higher quote.

And if all three offers come back high, the answer might not be a different lender. It might be 90 days of focused credit work: paying revolving balances down below 30% utilization, letting recent inquiries age, and reapplying. The Bankrate April 2026 average APR for a 700 FICO, 36-month, $5,000 loan was 12.27%. If you are being quoted significantly above that, your file probably has a story the model does not like, and credit work will move the rate more than shopping will.

Your right to a risk-based pricing notice

Under FCRA Section 615(h) and Regulation V, a lender that gives you a worse rate than its best customers, based on a credit report, has to tell you. The notice can take the form of a risk-based pricing notice or a free credit score disclosure. Most borrowers never read it. Read it. It tells you which credit bureau the lender pulled, your score from that bureau, and where you sit relative to the lender's other applicants. That is real information you can use to challenge an offer or shop a different lender. If a denial letter follows, the same logic carries through to the adverse action notice and your FCRA rights.

A short note on credit unions

The 18% NCUA cap on federally chartered credit unions is one of the most underused facts in consumer lending. A 660-FICO borrower being quoted 24% to 28% by fintechs may be quoted 14% to 17% by a credit union they joined that morning. Membership at most credit unions costs $5 to $25 and takes about ten minutes online. If your fintech offers are above 20%, the credit union check is not optional.

Why this matters for your borrowing decision

Three offers on the same day with a 15-point spread is not a sign that two of the lenders are wrong. It is a sign that pricing in this market is the sum of decisions made by humans (about cost of funds, target tier, marketing posture) and decisions made by models (about your file specifically). You cannot change the lender's cost of funds. You can change which lenders you put your file in front of, what loan purpose and term you ask for, and whether you take advantage of autopay or member rates. That is where the dollars live.

Frequently Asked Questions

Why do two lenders quote me different APRs with the same credit score?

Each lender uses its own risk model, has its own cost of funds, and targets a different segment of borrowers. Your FICO is one input among many, and lenders weight everything else (utilization, file depth, DTI, loan purpose, term) differently. The CFPB classifies this as risk-based pricing and it is permitted under federal law.

Does loan purpose actually change my rate?

Yes. Most lenders treat loan purpose as a pricing input. Debt consolidation typically prices below "major purchase" or "other" because consolidation borrowers, on average, have repaid more reliably in lender data. Always answer truthfully; misrepresenting loan purpose is fraud.

Should I always pick the lowest APR?

Pick the lowest APR after confirming it includes any origination fee (APR under TILA must include it, but verify on the disclosure), checking the total of payments, and reading the amount financed. A 9.99% loan with a 6% fee can cost more than a 13% no-fee loan over 36 months.

Why do credit unions often beat fintech rates?

Federally chartered credit unions are capped at 18% APR by NCUA rule on most consumer loans, fund lending from member deposits, and operate as nonprofits. The combination produces lower advertised rates for borrowers who would otherwise see 20%-plus offers from fintechs.

What is a risk-based pricing notice?

It is a disclosure required under FCRA Section 615(h) when a lender uses your credit report to give you materially less favorable terms than its best customers. The notice tells you which bureau was pulled and your score with that bureau. Lenders often satisfy the requirement by sending a free credit score disclosure instead.

How much can rates vary across lenders for the same borrower?

SoFi's published guidance says spreads can exceed 12 percentage points across lenders for the same applicant. Real spreads in 2026 sometimes run higher, particularly in the 660 to 720 FICO band where lender models disagree most.